ATP Prize Money vs Taxes: How Fiscal Residency Reshaped Modern Tennis

How ATP prize money and off-court income interact with tax residency, and why a generation of top players is publicly reported as resident in low-tax jurisdictions.

For four decades, the map of professional tennis has been split between two geographies: the cities where the tournaments are played (Wimbledon, Roland-Garros, the US Open) and the jurisdictions where, according to public residency records, many top players choose to live.

Over the last forty years, the legal choice of fiscal residency has become a routine part of an elite tennis career, in the same way that nutrition science or biomechanical coaching has. A review of publicly available residency declarations and ATP/WTA records suggests a clear pattern: as players climb the rankings, they are more frequently reported as residents of jurisdictions with low or no personal income tax.

How concentrated is tennis in low-tax jurisdictions?

Based on publicly reported residency information:

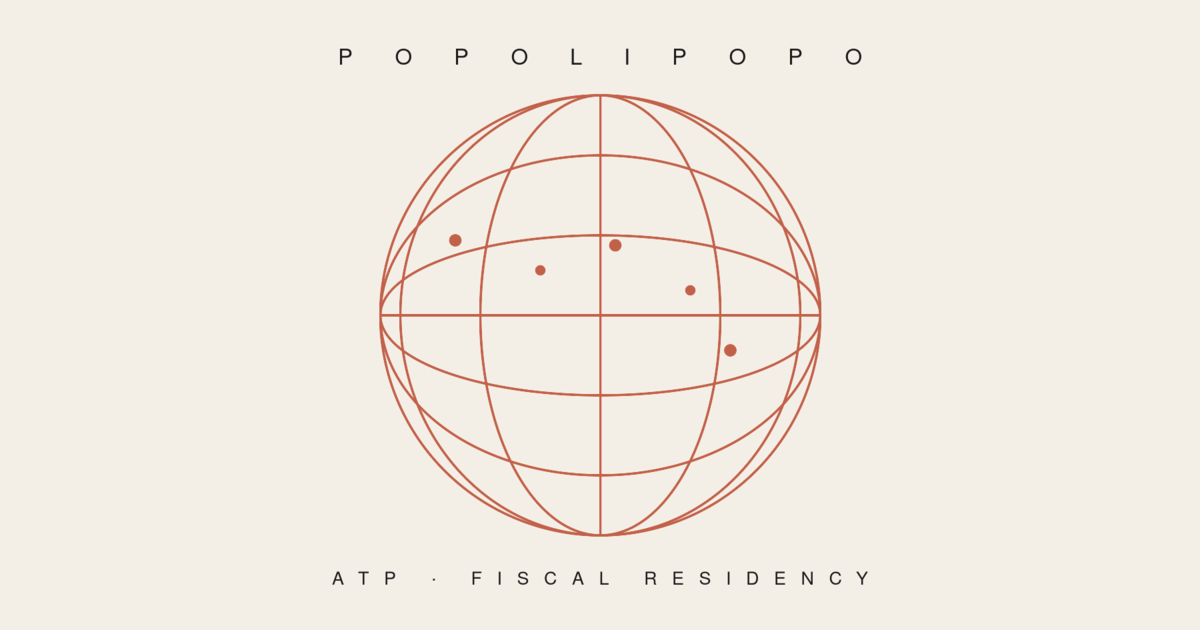

- Top 10 density. At various points over the last fifteen years, a majority of the ATP Top 10 has been reported as resident in low-tax jurisdictions. In 2024, several members of the men's Top 10 are publicly reported as residents of Monaco.

- The forty-year shift. In the early 1980s, only a handful of icons (such as Björn Borg) were publicly associated with Monaco. By the 2000s, choosing a low-tax jurisdiction had become a widely reported career pattern. According to public residency information and press reporting, an estimated 35% to 45% of the combined ATP/WTA Top 100 is now based in territories such as Monaco, the United Arab Emirates, the Bahamas or Switzerland.

Why are tennis players treated differently from team-sport athletes?

Unlike footballers or basketball players, whose salaries are typically paid by a club and taxed at source, professional tennis players are generally classified as independent contractors. They directly bear the cost of global travel, coaching, physical preparation, medical staff and accommodation. For a player ranked around No. 50 in the world, public estimates regularly place these annual operating costs above USD 250,000.

A key distinction matters for the tax debate:

- On-court prize money is generally taxed at source. The country hosting the tournament withholds a portion of the cheque. The UK, for example, withholds tax on Wimbledon prize money.

- Off-court income (sponsorships, image rights, licensing deals) is typically taxed in the player's country of fiscal residence.

That distinction is what makes fiscal residency a recurring topic of public debate. For a player such as Roger Federer, publicly reported as a resident of Switzerland, or Novak Djokovic, publicly reported as a resident of Monaco, the choice of residence influences how their off-court income is taxed. Whether this is the players' primary motivation is something only they can confirm. In their public statements, several have cited training infrastructure, climate and family proximity rather than tax rates.

Which jurisdictions are most often associated with top players?

- Monaco. A 0% personal income tax regime and a dense community of professional athletes. Players publicly reported as Monaco residents over the years include Boris Becker (later the subject of a separate German tax case unrelated to his Monaco residence) and Jannik Sinner.

- United Arab Emirates (Dubai). Often mentioned in connection with year-round training conditions and a 0% personal income tax. Roger Federer's longstanding training base in Dubai is widely cited as a template.

- The Bahamas. Reported as the residence of several Australian and Canadian players.

- Switzerland. Because of a specific 1963 tax treaty, French citizens who relocate to Monaco generally remain liable for French income tax. Switzerland, by contrast, offers the Forfait Fiscal (lump-sum taxation), a regime explicitly recognised in Swiss federal and cantonal law. It has historically been the most-reported jurisdiction of residence for top French players. See our deep dive on the Forfait Fiscal for athletes.

Are there notable exceptions?

Yes. Rafael Nadal is one of the most prominent players to have publicly maintained Spanish tax residency, citing his academy and family ties in Mallorca. In other countries, the residency choices of high-earning athletes have prompted public debate. Coverage of these debates varies widely in tone, and several players have publicly explained their choices in interviews.

As prize money and sponsorship values grow, the question of where elite players are taxed has become a recurring subject in sports-business journalism. None of this implies wrongdoing on the part of any individual player: residency is a legal status, declared to and accepted by the relevant tax authorities.

For the French case specifically, and the historical reasons French players were reported in Switzerland rather than Monaco, see our companion piece on French tennis player fiscal residency.

Editorial disclaimer. This article does not allege illegal conduct by any player named. It discusses publicly reported information (official residency declarations, court rulings, public statements, and ATP/WTA records) and the broader public-policy debate around the tax residency of professional athletes. Income, savings and tax figures attributed to individual players are independent estimates based on publicly available data, not declarations made by the players themselves. Where a player has chosen a particular jurisdiction of residence, that choice is, in itself, lawful.

All financial figures attributed to individual players are independent estimates based on publicly available data: ATP prize-money records, public reporting of endorsement partnerships, statutory tax rates published by Service-Public.fr, historical rates from the Institut des Politiques Publiques (IPP), and the official documentation of the Swiss Forfait Fiscal regime published by the Swiss Federal Tax Administration (ESTV) and individual cantonal tax offices. They are not declarations made by the players concerned and do not constitute tax advice.

Sources

ATP and prize-money records

- ATP Tour — official player profiles and career prize-money records. https://www.atptour.com/

French tax law and rates

- Service-Public.fr — current French income-tax brackets (Direction de l'information légale et administrative). https://www.service-public.fr/particuliers/vosdroits/F141

- Institut des Politiques Publiques (IPP) — historical tax-benefit calculator and rate series. https://www.ipp.eu/en/tools/tax-benefit-calculator/income-tax/

Swiss Forfait Fiscal (lump-sum taxation)

- Swiss Federal Tax Administration (ESTV) — official documentation of l'imposition d'après la dépense. https://www.estv.admin.ch/estv/en/home/allgemein/steuerstatistiken/fachinformationen/steuerbelastung/aufwandbesteuerung.html

Method note

All financial figures attributed to individual players in this article are independent estimates derived from public ATP prize-money records and public reporting of endorsement partnerships, combined with statutory tax rates published by the sources above. They do not reflect actual declarations made by the players, which are protected by Swiss and French tax secrecy. This article does not allege illegal conduct by any player named.